2 BHK vs 3 BHK: The Decision Framework Indian Families Keep Getting Wrong

Buy for the family you'll have in ten years - not just the one sitting at the dining table today.

The 2 BHK versus 3 BHK question feels simple, which is exactly why so many families get it wrong. They look at who's living with them right now, pick the size that fits today, and sign.

But a home is a 15-to-20-year decision, and families change far more than budgets do over that time. The smarter approach isn't to ask "what do we need now?" but "what will we need over the life of this home and what can we comfortably afford?" This framework walks you through both halves of that question.

Why the obvious answer is often wrong

Most buyers anchor entirely on their present situation: a young couple buys a 2 BHK because it's just the two of them; an established family stretches for a 3 BHK because the house feels full today. Both can be mistakes. The couple may have children and ageing parents moving in within a few years. The established family may be overpaying for space that empties out as children leave for college. The fix is to think across a decade, not a moment.

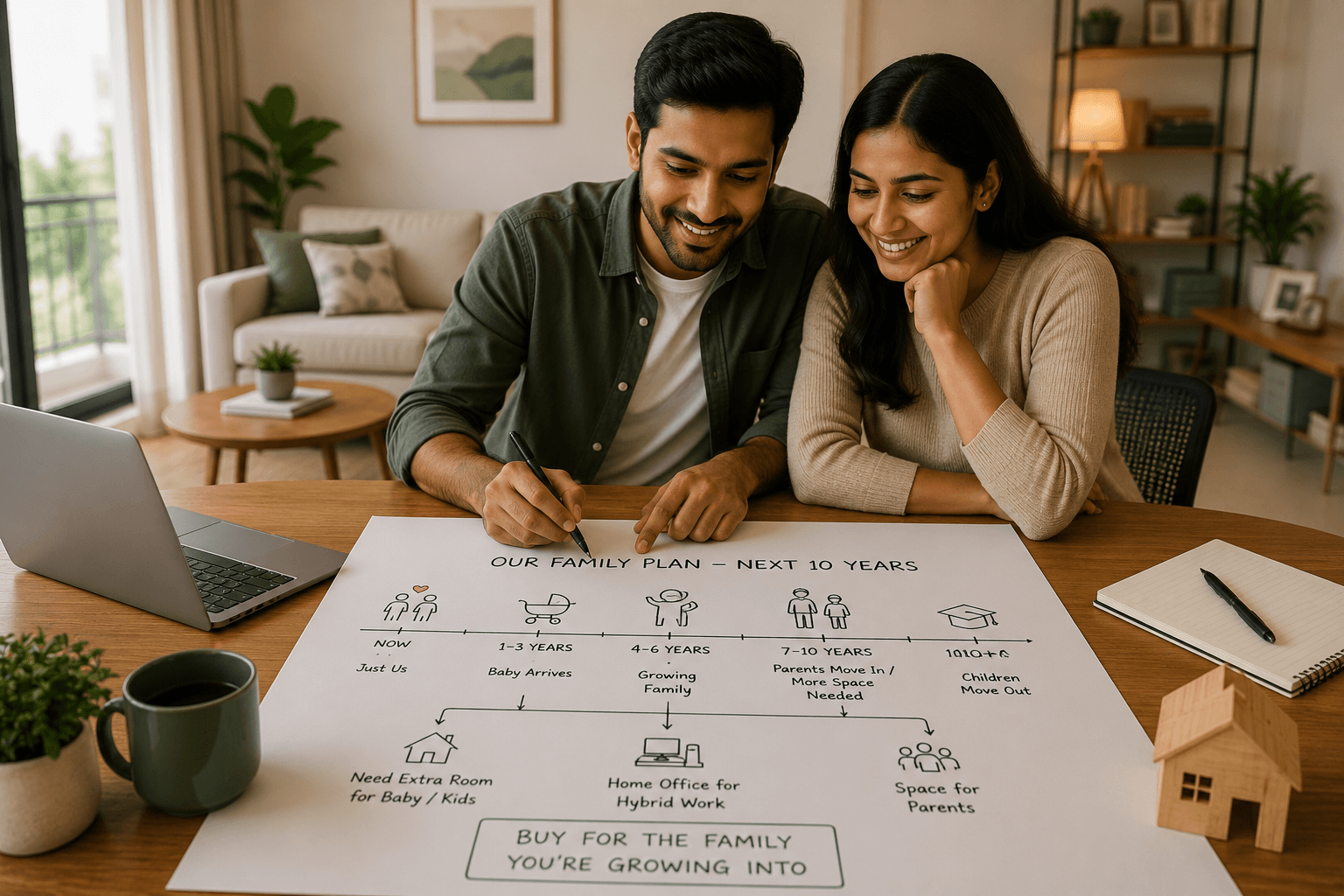

1. Map your family across the next 10 years

Sketch out the realistic life changes ahead: children arriving, parents moving in to live with you, a child growing into needing their own room, or children eventually moving out. Will you need a home office, now that hybrid work is common? A 2 BHK that's perfect for a couple can feel cramped within three years of a child and a visiting grandparent. Buy for the household you're growing into, not just the one you have.

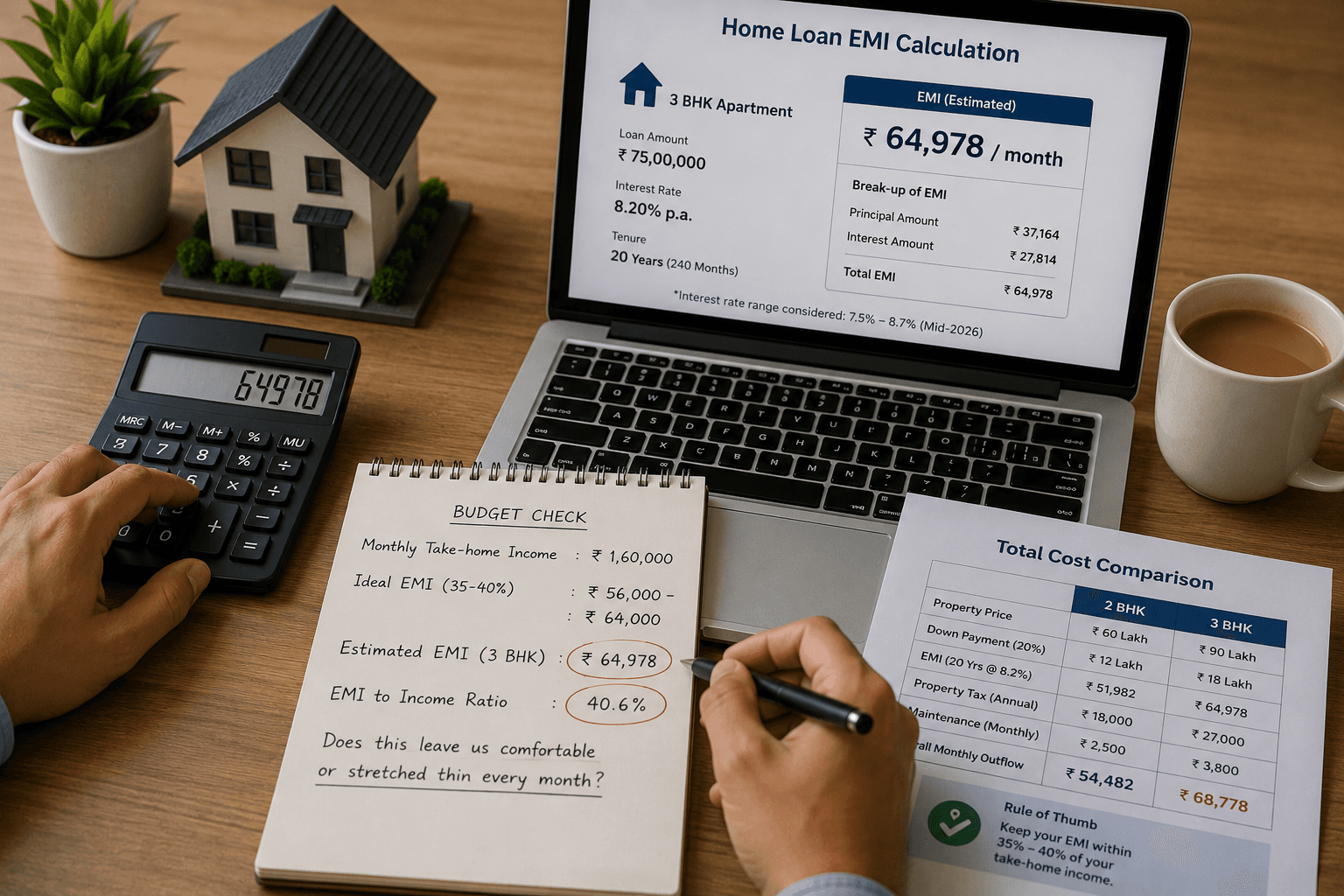

2. Stress-test the budget and EMI - honestly

A 3 BHK costs more across the board: higher price, larger down payment, bigger EMI, higher property tax, and more maintenance. The critical test is your EMI-to-income ratio. A widely used guideline is to keep your EMI within roughly 35–40% of your monthly take-home income and ideally lower, so you can still save and absorb shocks. Run the actual EMI for the 3 BHK at current rates (broadly 7.5%–8.7% in mid-2026) and ask honestly: does this leave us comfortable, or stretched thin every month?

A useful gut-check: if buying the 3 BHK means no emergency fund, no investments, and constant month-end anxiety, the 2 BHK isn't a compromise - it's the wiser choice. A home should add security to your life, not subtract it.

3. Don't forget the full cost of more space

The price difference is only the start. A larger home means higher recurring costs for years: maintenance charges (often per square foot), property tax, electricity for more rooms, furnishing, and upkeep. Factor these into your monthly budget, not just the purchase price. Sometimes a well-located 2 BHK costs far less to own and run than a 3 BHK in the same building - money you can invest or use to upgrade later.

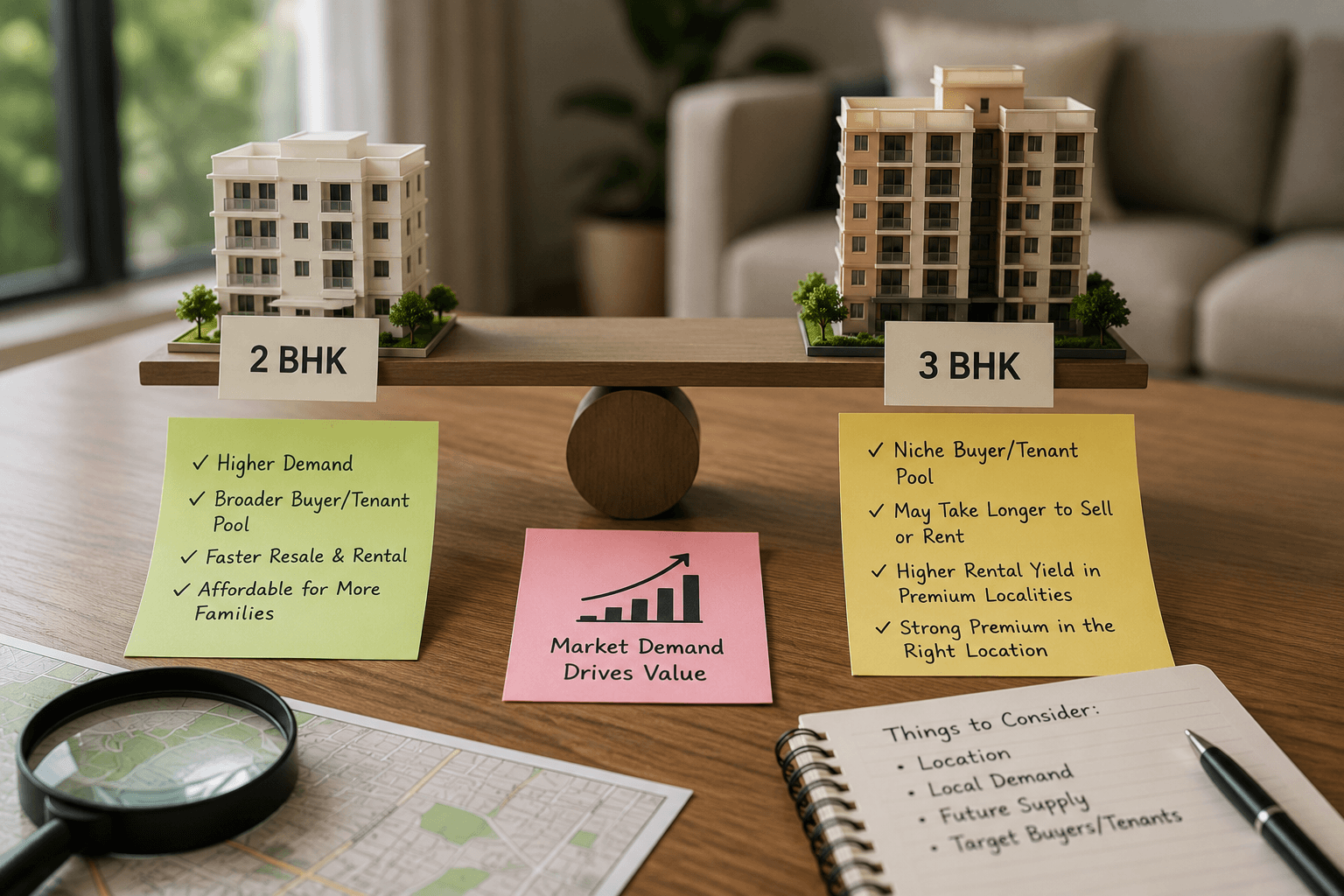

4. Weigh resale and rental demand

Think about the exit before you enter. In many Indian cities, 2 BHKs have the broadest pool of buyers and tenants — they're affordable for more families and easier to rent and resell. 3 BHKs appeal to a smaller, more affluent segment and can take longer to sell, but in premium or family-heavy localities they command a strong premium. Consider which configuration is in higher demand in your specific micro-market; that's what protects your investment if your plans change.

5. Consider the in-between options

The decision isn't always binary. A 2 BHK with a study or a convertible room can flex as your needs grow, often at a lower cost than a full 3 BHK. Some buyers find that a slightly larger 2 BHK in a better location beats a cramped 3 BHK in a worse one. And if your finances are likely to improve significantly in a few years, buying a comfortable 2 BHK now and upgrading later can be smarter than over-leveraging today.

A simple way to decide

Lean 3 BHK if your family is clearly growing, you'll need space for parents or a home office, the EMI sits comfortably within ~35–40% of take-home income, and 3 BHKs hold strong demand where you're buying.

Lean 2 BHK if your household is stable or the future is uncertain, the 3 BHK EMI would stretch you, you value financial breathing room, or you're prioritising a better location over raw size.

The right size isn't the biggest you can technically qualify for, nor the smallest that fits today — it's the one that matches the family you're realistically going to be, at a cost that keeps you financially secure. Picture your household ten years out, run the EMI honestly, account for the full cost of ownership, and think about resale. Do that, and the 2-versus-3 BHK question stops being a guess and becomes a clear, confident decision.

Buy smarter with Wishki. Wishki helps you explore 2 BHK and 3 BHK options across projects and talk to families who made the same call - so you can pressure-test your decision against real experience before you coit.

This article is for general information only and is not legal, financial, or tax advice. Loan rates, tax rules, and GST applicable to your purchase change over time and vary by lender, state, and your individual circumstances - please verify current details and consult a qualified professional before deciding.

Recent Posts

Home Loan ke 10 Terms Jo Aapko Samajhni Hi Chahiye - Before You Sign

2026-06-30T13:06:49.880Z

Location, Location, Location: The 8 Questions to Ask Before Buying in Any Area

2026-06-24T11:08:06.371Z

Best Real Estate Investment Cities in India for 2026

2026-05-28T11:01:24.527Z

Cost Overruns in Construction: Causes and Solutions

2026-04-28T13:08:00.074Z

Step-by-Step Guide to Buying Your First Property

2026-04-28T12:02:47.860Z