Home Loan ke 10 Terms Jo Aapko Samajhni Hi Chahiye - Before You Sign

Bank jargon decoded in plain language, so you don't sign away lakhs without realising it.

A home loan is probably the largest financial commitment you will ever make - often 20 to 30 years long. Yet most buyers sign the agreement understanding barely half the terms in it. Banks rarely lie, but they do rely on jargon, and a buyer who doesn't understand the fine print usually accepts worse terms without even knowing. The difference between an informed and an uninformed borrower on a single loan can run into several lakhs. Here are the ten terms you must understand before you sign anything.

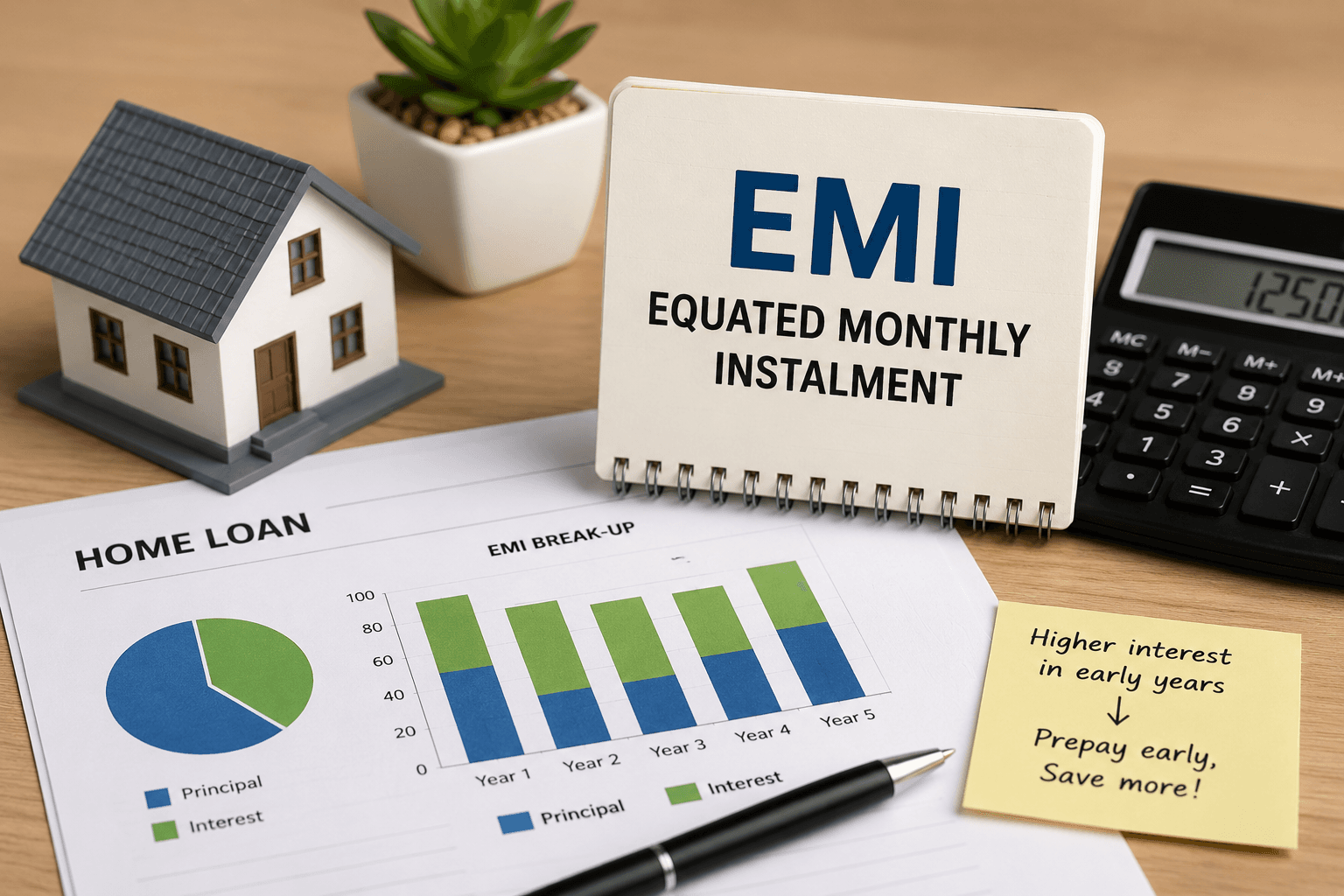

1. EMI (Equated Monthly Instalment)

Your fixed monthly payment to the bank, made up of two parts: principal (the actual loan amount) and interest. In the early years, most of your EMI goes toward interest and very little toward principal — which is exactly why prepaying early saves so much. Always ask for the full amortisation schedule so you can see this split year by year.

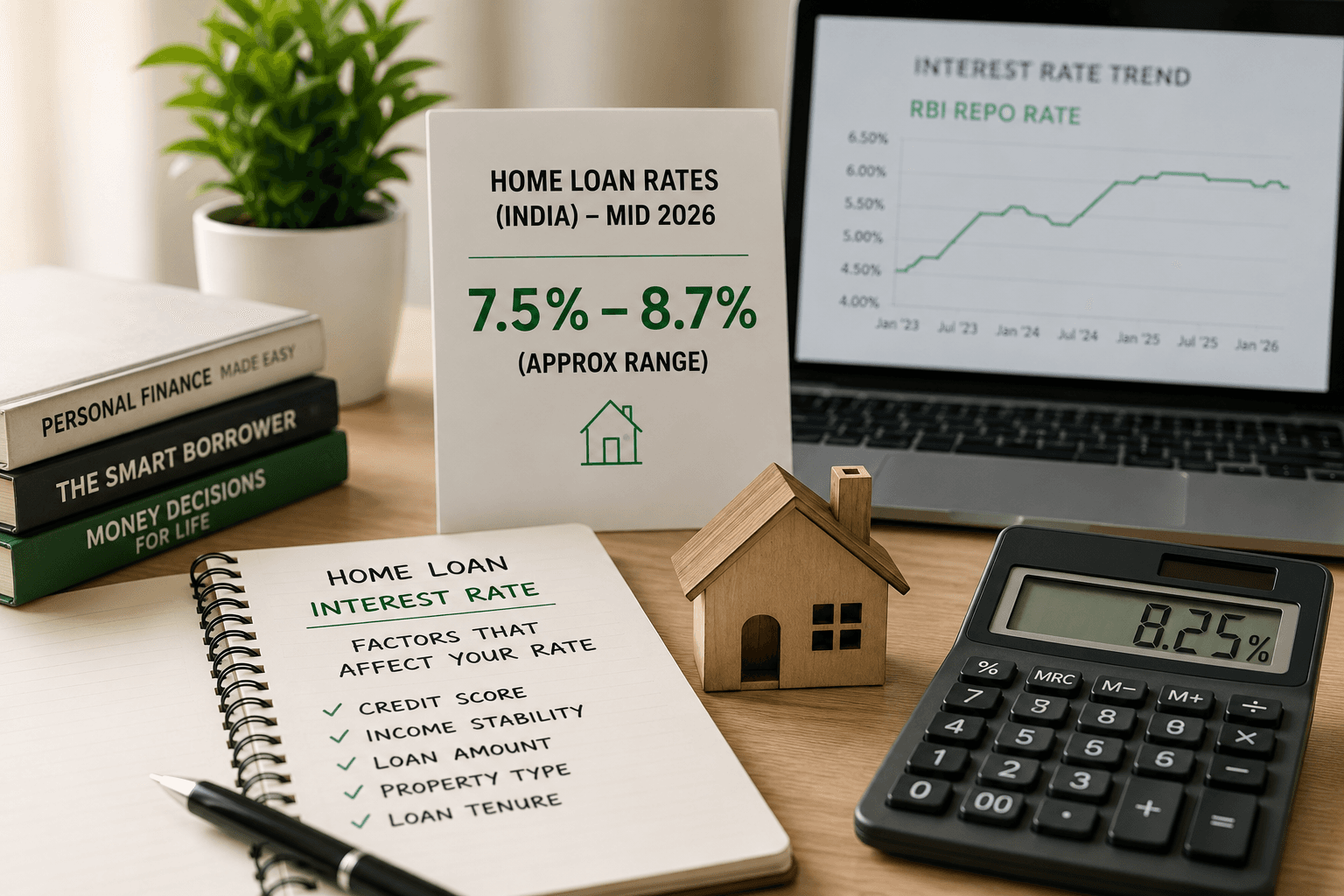

2. Interest rate — and what drives it

As of mid-2026, home loan rates in India broadly range from about 7.5% to 8.7%, with the best rates going to borrowers with strong credit scores. Your rate is not random — it depends on your credit score, income stability, loan amount, the property, and tenure. Even a 0.25% difference is significant: on a ₹50 lakh loan over 20 years, it can mean lakhs over the life of the loan. Never accept the first rate quoted; it is often negotiable.

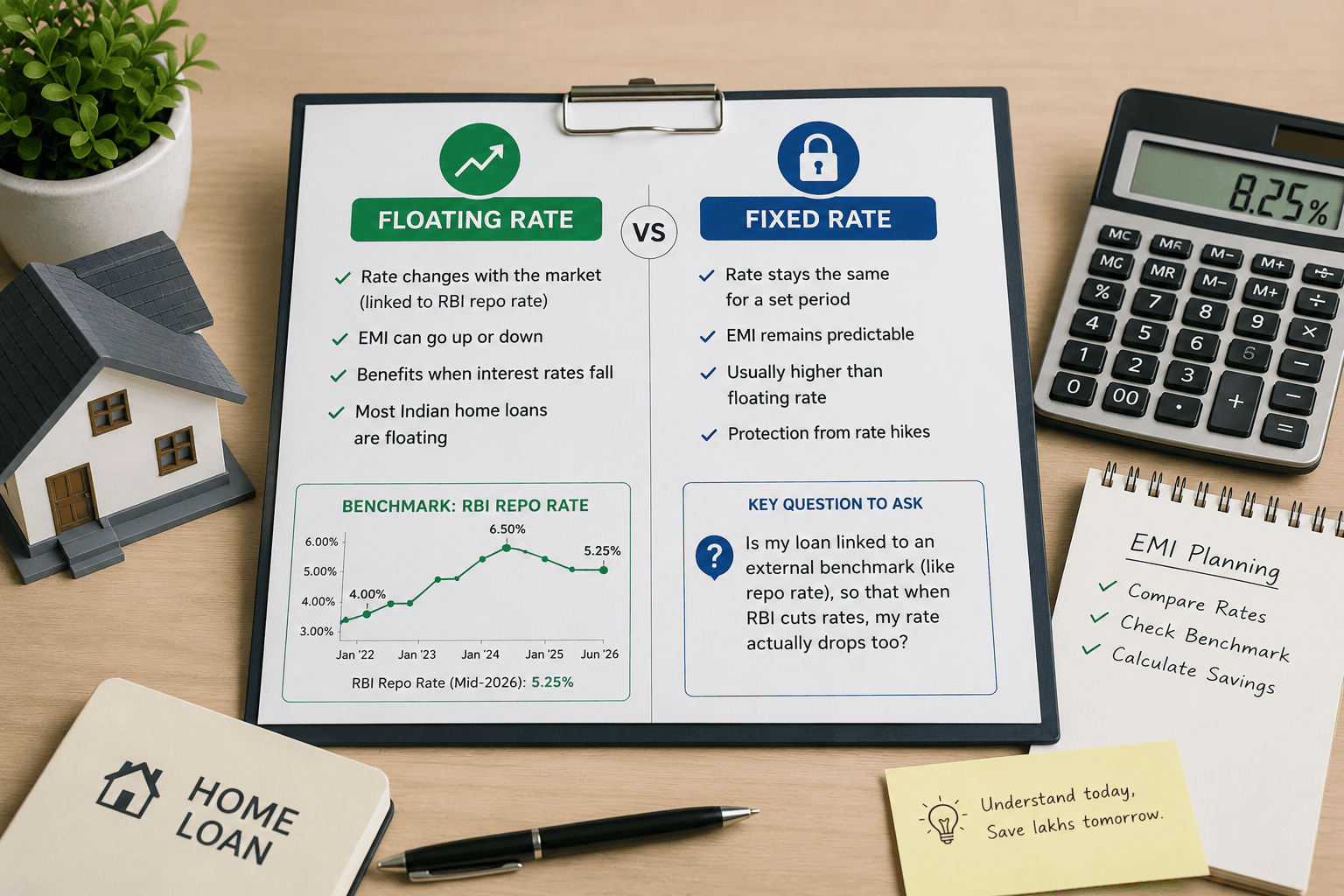

3. Floating vs. fixed rate

A fixed rate stays the same for a set period - predictable EMIs, but usually higher to start. A floating rate moves with the market (linked to the RBI repo rate, which stood at 5.25% in mid-2026), so your EMI can rise or fall. Most Indian home loans are floating. The key question to ask: is my loan linked to an external benchmark (like the repo rate), so that when the RBI cuts rates, my rate actually drops too?

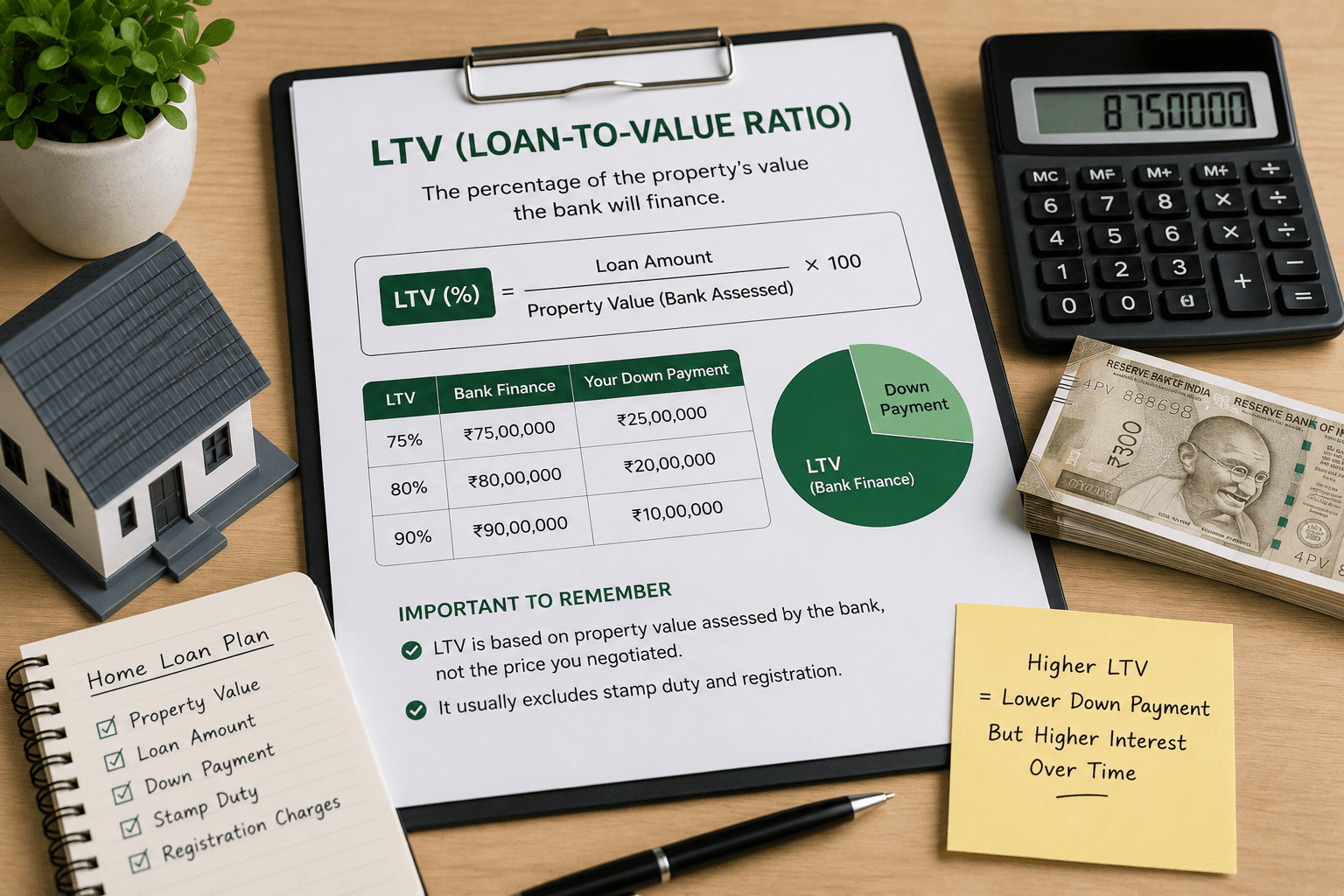

4. LTV (Loan-to-Value ratio)

The percentage of the property's value the bank will finance — typically 75% to 90%. The rest is your down payment, which you must arrange yourself. A higher LTV means a smaller down payment but a larger loan and more interest overall. Remember: LTV is calculated on the property value the bank assesses, not the price you negotiated, and it usually excludes stamp duty and registration.

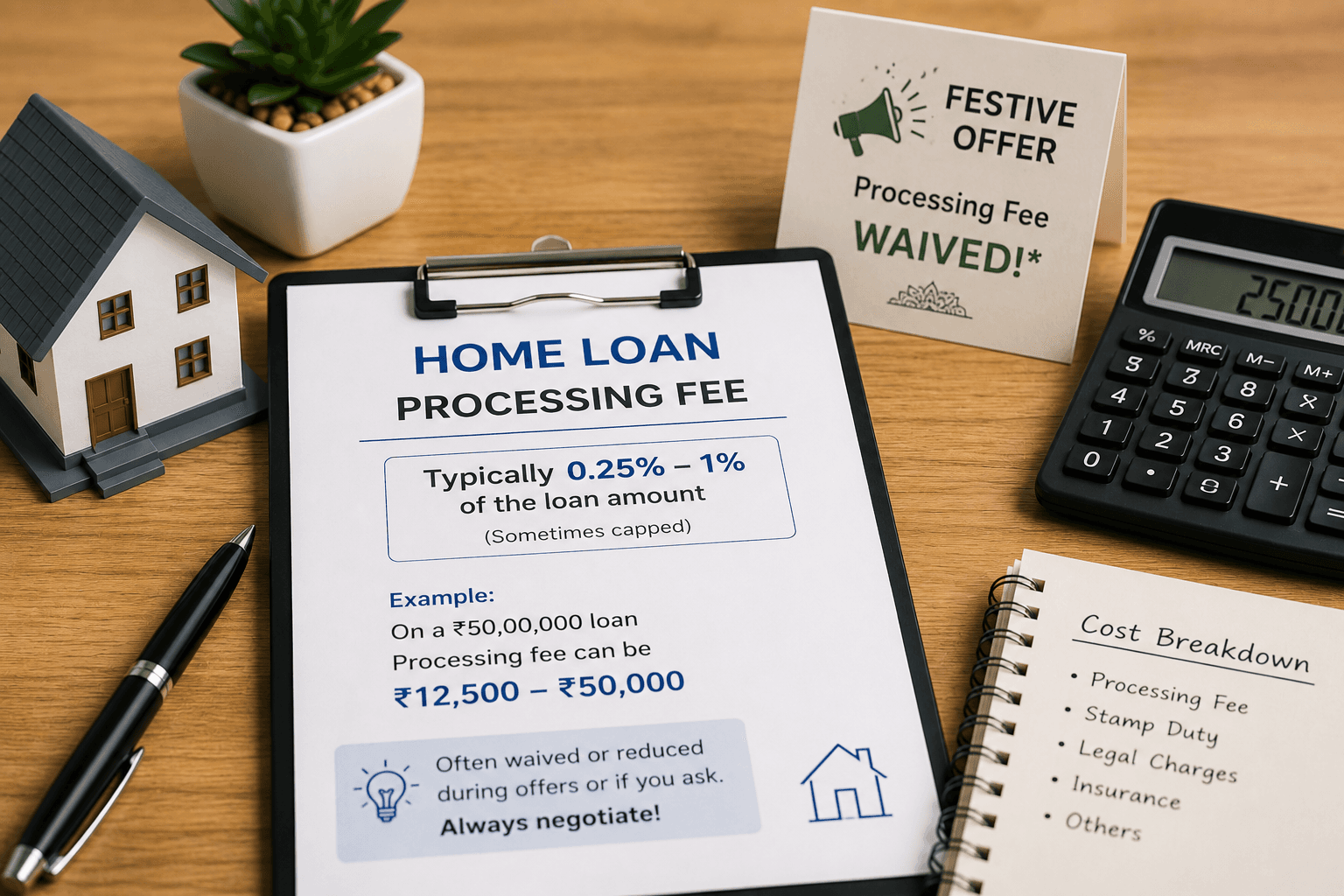

5. Processing fee

A one-time charge for handling your application, generally around 0.25%–1% of the loan amount (sometimes capped). On a ₹50 lakh loan that can be tens of thousands of rupees. It is frequently waived or reduced during festive offers or if you simply ask - so always negotiate it.

6. Prepayment / foreclosure

Paying off part or all of your loan ahead of schedule. For floating-rate home loans to individuals, the RBI does not allow banks to charge prepayment or foreclosure penalties — a powerful right many borrowers don't use. Prepaying even small amounts in the early years, when interest dominates your EMI, dramatically reduces your total interest. (Fixed-rate loans may still carry a charge, so confirm.)

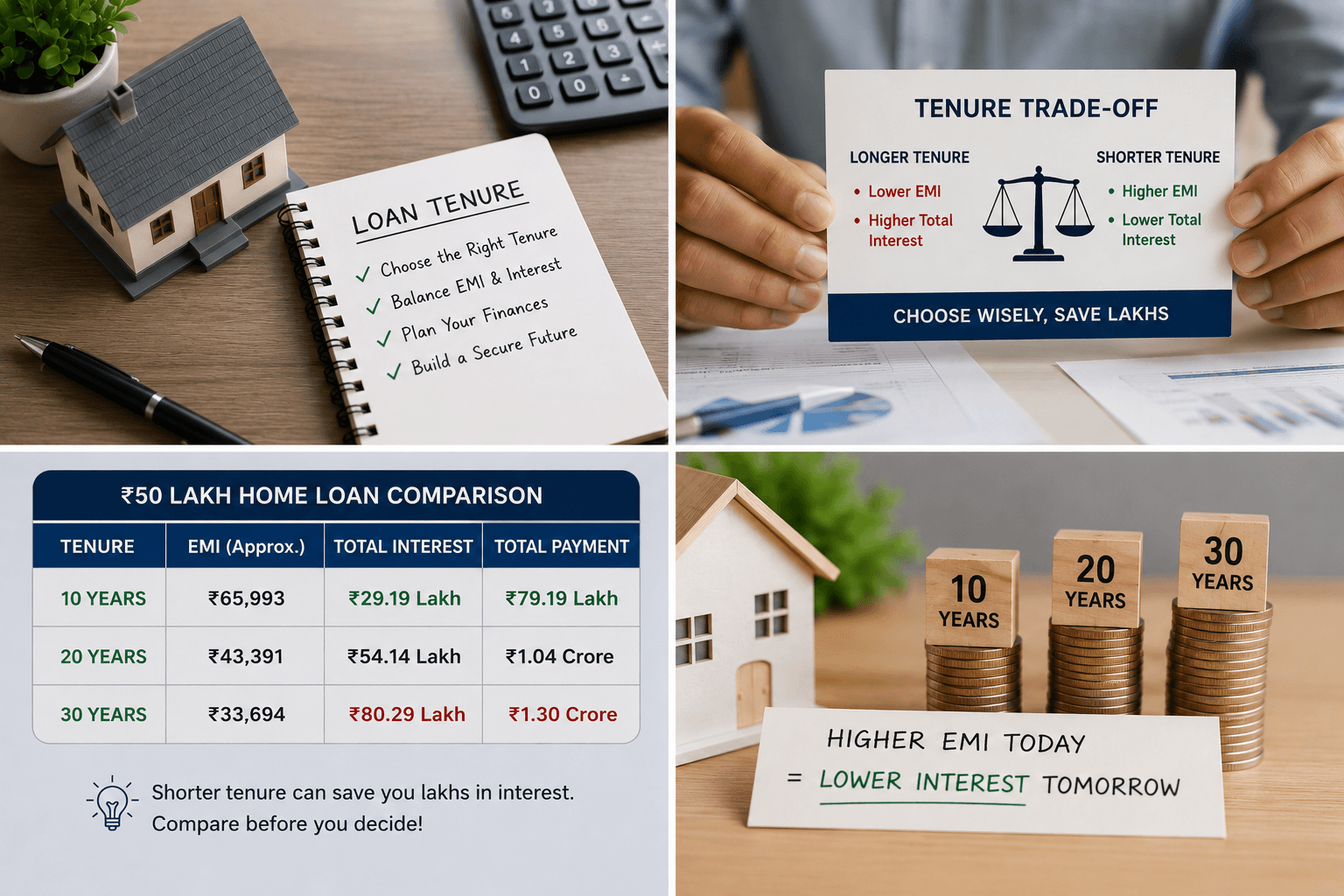

7. Tenure

The length of your loan. A longer tenure lowers your monthly EMI but sharply increases total interest paid; a shorter tenure means a higher EMI but far less interest overall. Don't choose the longest tenure just to make the EMI look comfortable — model a couple of options and see the lifetime cost.

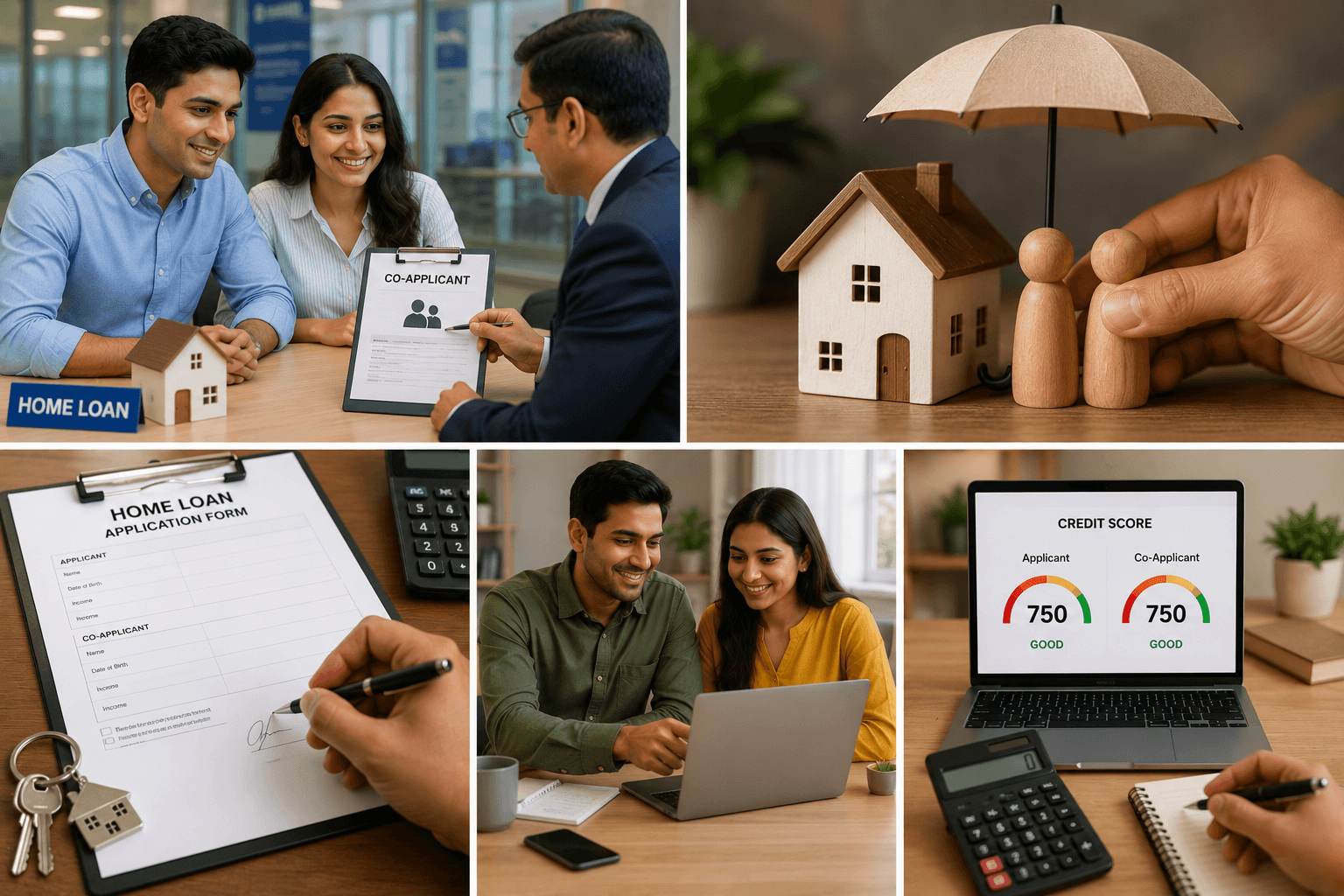

8. Co-applicant

A second person on the loan — usually a spouse or parent. Adding a co-applicant with income can increase your eligibility and, if both are co-owners, both can separately claim tax deductions on the same loan (up to the individual limits). But a co-applicant is equally liable for repayment, and any default hurts both credit scores. Choose deliberately, not casually.

9. Amortisation schedule

The full table showing how each EMI splits between principal and interest across the entire tenure, and how your outstanding balance shrinks. It is the single most useful document for planning prepayments and understanding what you actually owe at any point. Ask for it in writing before you sign — not after.

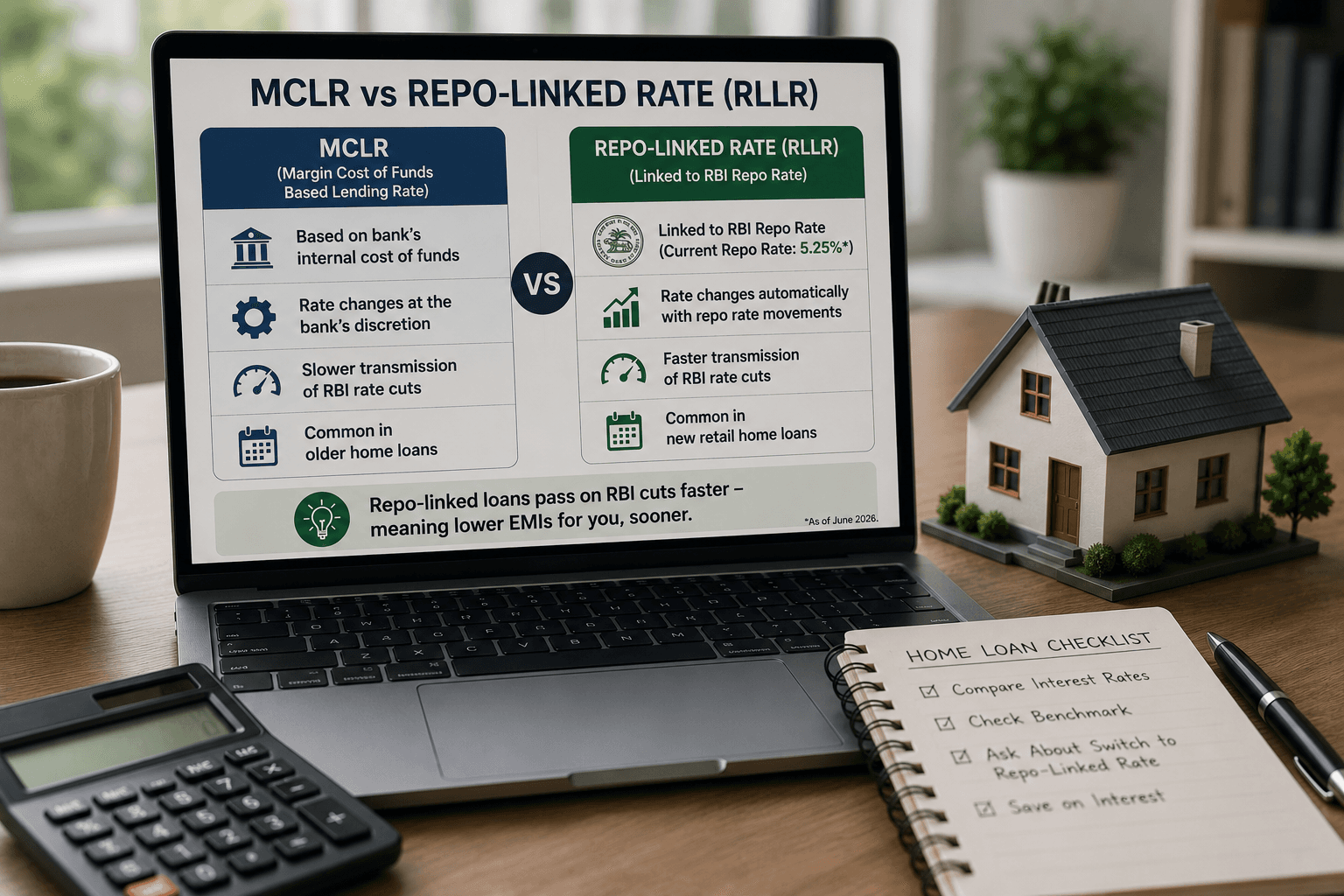

10. MCLR, repo-linked rate, and the benchmark

Floating rates are tied to a benchmark. Older loans used MCLR (the bank's internal cost of funds); newer retail loans are usually repo-linked (RLLR), which moves transparently with the RBI's repo rate. Repo-linked loans pass on RBI cuts faster. If you have an older MCLR loan, it is worth asking your bank to switch you to a repo-linked rate.

Two questions that protect you

Before signing, ask the lender two things in writing: "What is the all-in cost — interest plus every fee?" and "What can change over the life of this loan, and when?" Honest answers to those two questions surface almost every hidden cost. An informed borrower isn't an aggressive one — they're simply someone the bank can't quietly overcharge.

Buy smarter with Wishki. Wishki helps you compare loan-linked projects and connect with buyers who've recently financed similar homes - so you walk into the bank already knowing the right questions to ask.

This article is for general information only and is not legal, financial, or tax advice. Loan rates, tax rules, and GST applicable to your purchase change over time and vary by lender, state, and your individual circumstances — please verify current details and consult a qualified professional before deciding.

Recent Posts

Location, Location, Location: The 8 Questions to Ask Before Buying in Any Area

2026-06-24T11:08:06.371Z

2 BHK vs 3 BHK: The Decision Framework Indian Families Keep Getting Wrong

2026-06-23T13:18:52.638Z

Best Real Estate Investment Cities in India for 2026

2026-05-28T11:01:24.527Z

Cost Overruns in Construction: Causes and Solutions

2026-04-28T13:08:00.074Z

Step-by-Step Guide to Buying Your First Property

2026-04-28T12:02:47.860Z